Summary

1) The economy has defied expectations and avoided recession for several quarters because the Fed has injected new liquidity into the financial system despite hiking interest rates.

2) The economy will fall into a recession in the coming quarters due to a combination of headwinds. They include:

A) The natural cooling of the economy when the last embers from Jay Powell’s monetary bazooka shots at the Pandemic and the series of regional bank failures (the Bank Term Funding Program) finally burn out.

B) “Something breaking” in the current higher-rate environment. Possibilities include a correction of the housing market if rising unemployment causes a break in the impasse between supply and demand, a cascade of commercial real estate and/or auto loan defaults, another cascade of regional bank failures, and black swans in the financial system caused by domestic bond default contagion or contagion from foreign sources such as an ailing Chinese economy.

Side note: The economic impact of back swans not caused by rate hikes, such as tensions in the Middle East, a drought blocking the Panama Canal, or a United Auto Workers strike, could be magnified by the higher-rate environment, and inflationary pressures they create could make it difficult for the Fed to cut interest rates should such black swans occur.

C) Headwinds against discretionary spending from the resumption of student loan repayments in October.

D) A business and/or consumer credit crunch. (Both of which are well into the making.)

3) Valuations of unprofitable, heavily-indebted tech “zombie companies” have rocketed recently due to a combination of:

A) New monetary stimulus intended to stop the cascade of regional bank failures (BTFP) ultimately being funneled into “growth stocks”.

B) Irrational exuberance boosting the price of any company that has any connection to A.I., no matter how tenuous (reminiscent of the irrational exuberance of the Dot Com Bubble).

4) As interest rates remain elevated and the economy misses its “soft landing”, debt-ridden zombie companies, which were shown to be unprofitable during the best of times, will be forced to reorganize to continue to service their debt, severely diluting their equity. (And in some cases, wiping it out completely.)

5) Given the recent 1999ish “buy everything A.I.” run-up, now would be a fantastic time to start shorting these companies.

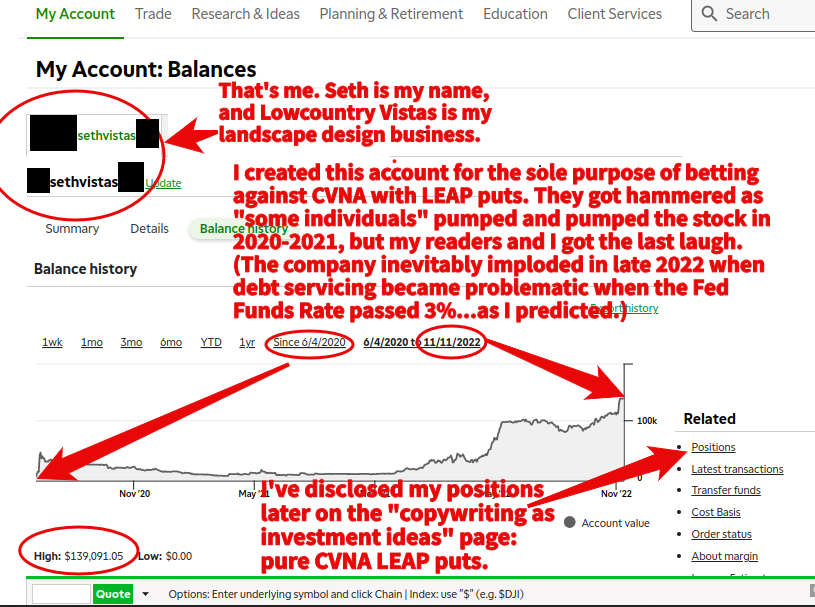

6) I’m currently short or have long-term puts against the following tech zombies: CVNA, W, and UPST…I’ll consider adding to these positions if they continue to squeeze.

Hunting zombies is a side gig, but I’m a pretty good hunter.

Although I’m not a professional trader, I have had great success trading the market’s return to post-pandemic economic reality. Notably, I earned several hundreds of percent (several tens of thousands of dollars for this middle-class guy) on LEAP puts against Carvana.

Given that I don’t have the letters “C.F.A.” behind my name and I’ve never worked for an advisory firm, I think the best way for me to build credibility as a trader is to show that my trades are profitable. Thus, I’m taking this opportunity to explain my current positions. (For what it’s worth, I’m also an M.B.A.)

As I just noted, in my last “big short”, long-term OTM puts against CVNA, I yielded hundreds of percent and tens of thousands of dollars…I’m confident that the combined profit from these “zombie killer” trades will rival that of my CVNA trade.

My “next big short” is going to take some explaining, so I’m going to break everything down into a series of posts. Right now, I just want to introduce my thesis and explain why I believe that the U.S. will go into recession soon.

The Recession that Never Comes (But Will!)

This trade is based on the premise that highly-indebted tech companies (particularly those that operate in the consumer discretionary space) that couldn’t pull a GAAP profit when everyone was sitting at home and pulling forward consumer demand with free money will face an existential crisis when the recession finally hits.

So, let’s start off by showing that a recession will finally hit.

Investing.com’s Lance Roberts (who, unlike me, has actually worked in asset management) recently noted that the economy may be avoiding the recession that nearly everyone has been expecting for what seems like forever because monetary stimulus remains high despite the Fed’s interest rate hikes.

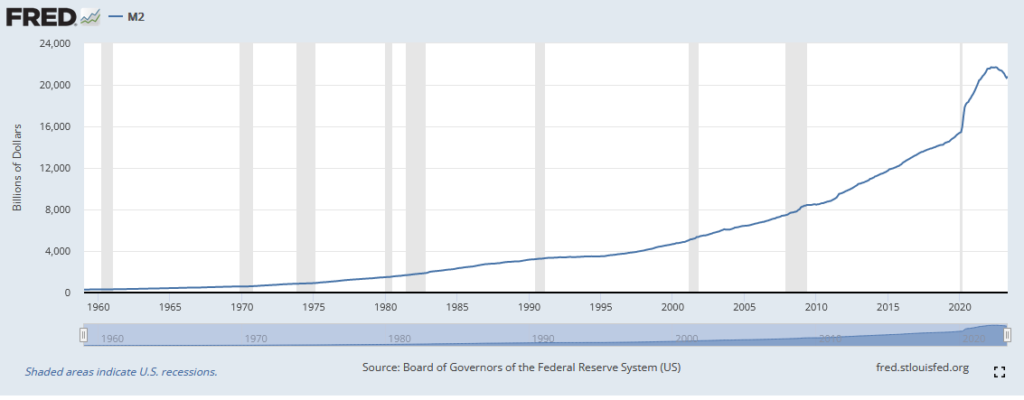

How much stimulus remains sloshing throughout the system? Well, here’s a historic chart of M2. Notice that the current level remains far from returning to the historic trendline.

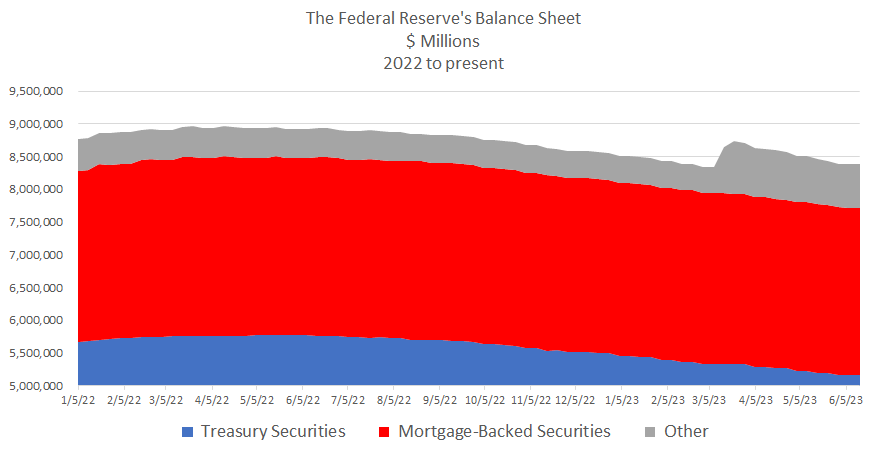

While the Fed has been swearing up and down that it’s conjured Paul Volcker and adopted monetary discipline, it’s soaked up but a tiny bit of the trillions in liquidity that it pumped during the pandemic. What’s more, following a string of regional bank failures earlier this year, it unleashed additional liquidity, as depicted by the gray line on the following chart:

Despite the hawkish stance Jerome Powell has been promoting in the financial media as of late, the Fed has been continuing to pump the financial system with liquidity, juicing economic data and stock prices alike.

But sugar highs are always fleeting. Notice that, while the Fed boosted liquidity following the regional bank failures this spring such that its balance sheet returned to early 2022 levels, quantitative tightening resumed shortly thereafter. Liquidity has since resumed its downward trajectory to the historic trendline, as seen on the previous charts of M2 and the Fed’s balance sheet.

Quantitative Tightening is well underway; it’s just that the decline in “easy money” started at a nosebleed level and has a long way to go to meet that trendline.

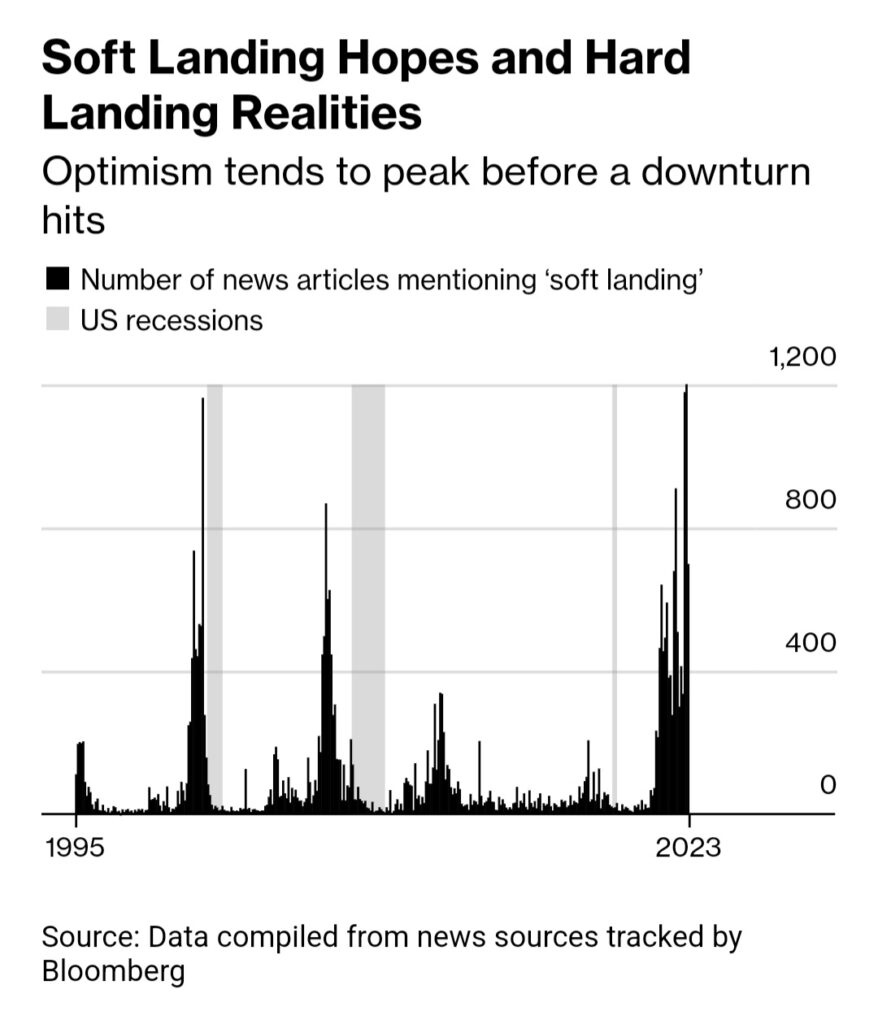

And let’s interject some common sense: You don’t go from 15 years of extraordinarily dovish monetary policy, including ZIRP and QE (which were considered “experimental” monetary policy tools following the GFC), to cyclically-high interest rates and QT without something breaking. A “soft landing” under these circumstances defies basic logic.

In fact, let’s look at the numerous, erroneous “soft landing” calls before the tech bubble recession and the GFC and compare them with the numerous calls for a “soft landing” in this historic return from off-the-charts dovish monetary policy. From Bloomberg:

So, how much longer until the recession finally arrives?

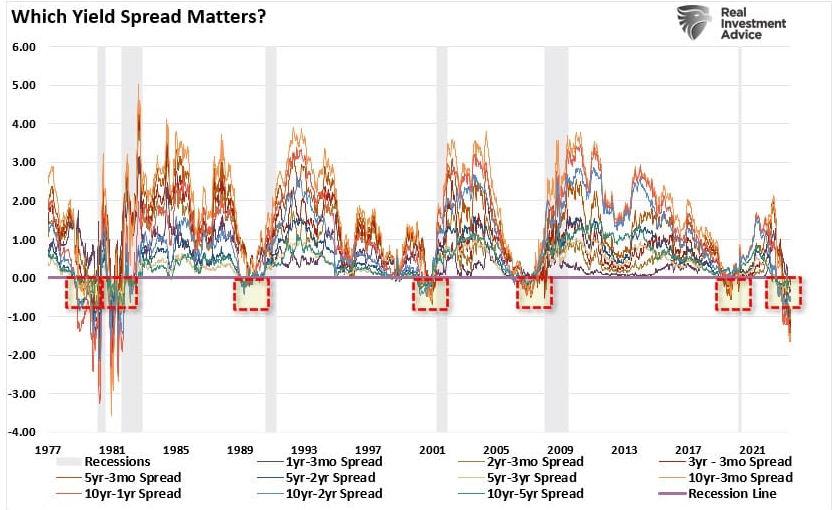

Well, yield curve inversion has only signaled a couple of false positives since the Great Depression, and it has had a perfect record of predicting recessions since the Carter Administration. All recessions since the mid 1970s have started after a continuous inversion of 6 quarters or less…we’re currently ending the 4th quarter since the beginning of the current inversion.

If the yield curve is to be trusted, the economy should fall into recession by Q1 or Q2 2024, economic headwinds that could shorten the timeline notwithstanding.

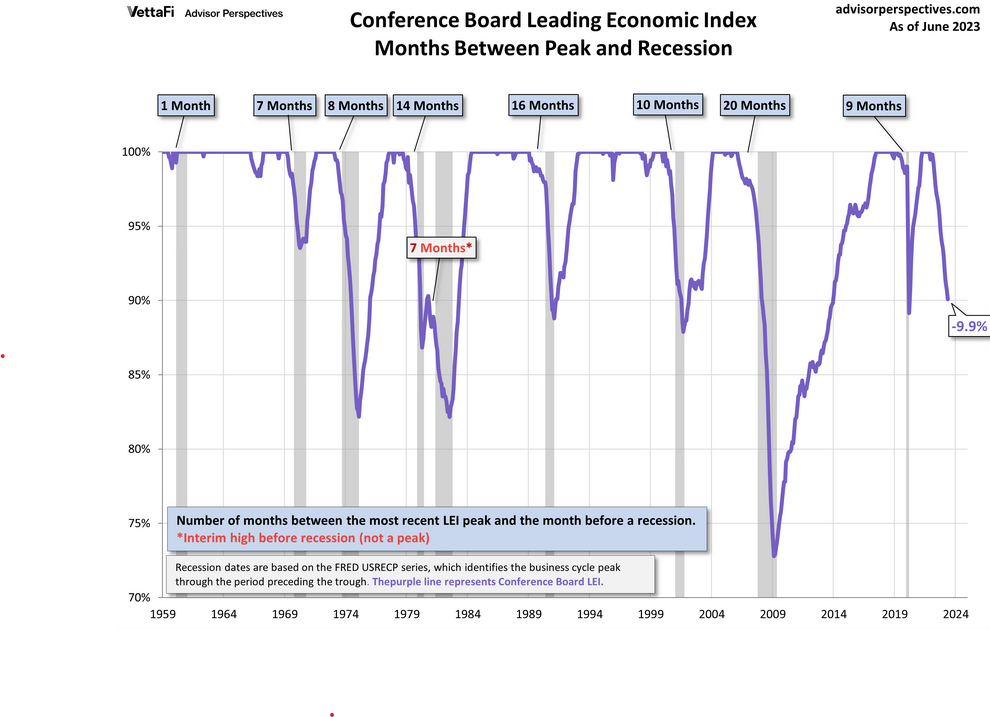

If the yield curve isn’t convincing enough of a recessionary indicator for you, then consider this: The “indicator of economic indicators”, the The Conference Board Leading Economic Index, which has had a near-100% accuracy rate of predicting recessions since its inception in 1959, is strongly suggesting that we’re heading into a recession in the coming quarters.

While some analysts believe that the current yield curve inversion’s prediction of recession may be distorted due to the fact that it’s happening at a time when historic monetary stimulus has been clashing with the fastest pace of interest rate hikes since the Volcker Fed, no one can deny the near-100% predictive power of the LEI, of which the yield curve is just one of several data points:

The depth and length of decline of the LEI suggest that a recession is coming soon to a country near you.

What’s next?

In Part 2 of this three-act saga, I’ll further explain why a zombie-killing recession is slowly ambulating toward us.

Then, in the final act, I’ll give juicy details about the zombies I’m hunting and my plans to slay them. (I might end up devoting an article to each of the 3 zombies.)

Until then, thanks for reading, and try to avoid feeding the zombies your hard-earned money like the Apes do!